What is Bicycle Insurance?

What you need to know about bicycle insurance - costs, cover options and how to keep your bike safe.

What you need to know about bicycle insurance - costs, cover options and how to keep your bike safe.

Bicycle insurance is a type of cover that protects you financially if your bike is stolen, damaged, or if you injure someone whilst out riding. You can get bicycle insurance as a standalone policy, or add it to your existing home insurance policy as an add-on. Depending on the level of cover you choose, it can protect against everything from bike theft and accidental damage through to personal accident cover and public liability cover.

At a glance

At a glance

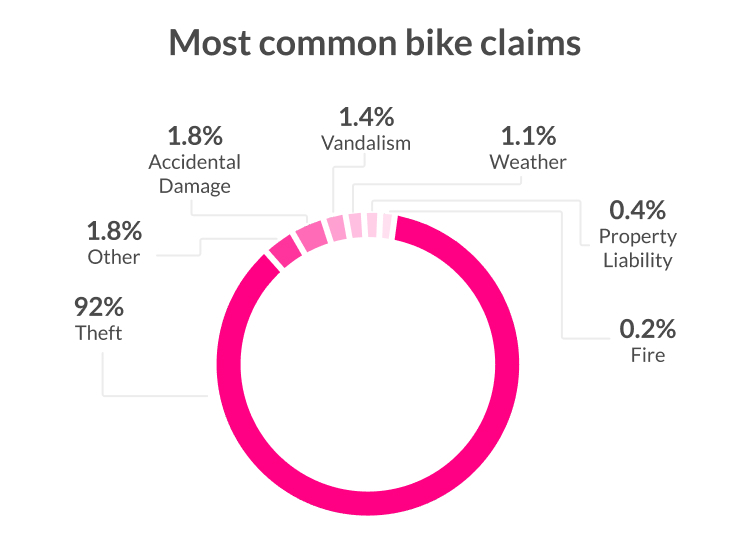

Bicycle insurance isn’t compulsory in the UK, but it’s a smart financial safety net. With nearly 15,000 cyclists injured on UK roads in 2023 and around 57,000 bikes stolen in 2024, the real figure is likely higher due to unreported thefts.

Being uninsured means covering those costs yourself. For anyone with an expensive bike or who simply relies on one to get around, a proper bicycle insurance policy is well worth having.

The level of cover you get depends on whether you opt for standard home insurance cover or a dedicated specialist bicycle insurance policy. Specialist policies typically include:

It’s always worth reading the policy wording carefully. Most bike policies won’t cover:

Yes, up to a point. Your bike is typically treated as part of your personal belongings under a home insurance policy, which means it’s covered for things like fire, vandalism and burglary whilst it’s at home.

But here’s the catch: standard home insurance cover usually only protects your bike within the boundaries of your home. The moment you ride it to the shops, park it outside your office, or take it on a weekend away, that cover may stop.

What to watch out for:

If you’ve got a high-value bike, it’s also worth adding it as a named high-value item on your policy. This ensures you’re covered up to the full value of your bike, rather than a generic single-item limit.

Pretty much any pedal-powered bike qualifies for bicycle insurance. Most bike policies cover:

Motorcycles and mopeds don’t count, these require separate motor insurance. And if your e-bike exceeds 15mph or requires compulsory motor insurance, it won’t qualify under standard bicycle insurance cover either. Check your policy wording if you’re unsure, or look for specialist electric bike insurance.

With e-bike popularity growing rapidly across the UK, they’re becoming an increasingly common sight on our roads. They’re also generally more expensive to repair and replace than regular bikes, which means a standard bicycle insurance policy may not fully cover the cost of an e-bike claim. Specialist electric bike cover is often the better choice.

When it comes to how an insurance company compensates you after a claim, there are two main approaches:

If your bike is less than three years old and was bought new, a new for old policy will replace it with an equivalent model at today’s prices, regardless of depreciation. Make sure the insured value reflects the current replacement cost, not what you paid at the time.

If your bike is more than three years old or was bought second-hand, your insurance provider will typically pay out based on its current market value, factoring in depreciation. This means you might receive less than you’d need to buy a direct replacement.

Always check which applies to your bicycle insurance policy before you buy.

Yes, and it can work out to be more affordable. Multi-bike policies let you cover multiple bikes under a single insurance policy, which means less admin and potentially a multi-bike discount compared with insuring each one separately.

You can usually add family members’ bikes too, as long as you all live at the same address. Handy if you’ve got a household full of cyclists.

Whether you’re topping up your home insurance policy or building out a specialist bicycle insurance policy, here are the add-ons worth thinking about:

| Add-on | What it covers |

|---|---|

| Accidental damage | Crashes, scrapes, and mishaps on the road |

| Theft & Loss | Essential for protection away from home |

| Personal accident cover | Pays out if you’re injured whilst riding |

| Public liability cover | Covers you if you injure someone or damage their property |

| Accessories cover | Helmets, lights, computers, and other kit |

| Worldwide cover | Cycling trips abroad or international races |

| Competitive use | Sportives, races, and timed events |

| Bike hire / cycle hire | A replacement bike whilst yours is out of action |

| Legal expenses | Legal costs following a personal injury dispute |

| Off-roading | Taking your mountain bike somewhere muddy and technical |

Some bicycle insurance providers include a few of these as standard and others offer them as paid add-ons. Always look at what’s included before committing to a policy.

Most cyclists pay between £3 and £25 a month for bicycle insurance, depending on the level of cover they need. A basic policy for a commuter bike sits at the lower end, whilst comprehensive cover for high-end road bikes or electric bikes will push towards the higher end.

Your exact insurance premium will depend on:

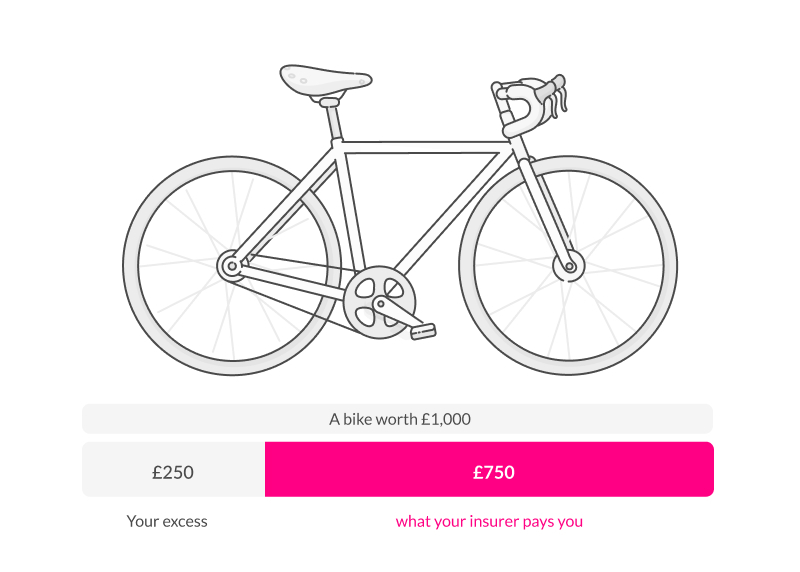

Top tip: If your excess is £150 and your bike is only worth £200, a claim might not be worth making. Make sure your excess is set at a sensible level relative to the value of your bike.

Bicycle insurance is your safety net, but prevention is always the better option. Here’s how to reduce the risk of bike theft and damage:

Always use a Sold Secure-rated bike lock. Not having one when your policy requires it could invalidate your claim, so don’t cut corners here.

Secure both wheels and the frame to an immovable object like a solid bike stand or lamppost. Some thieves will nick the frame and leave the wheels, or vice versa.

Leave your bike somewhere busy and well-lit. Thieves are less likely to strike where there are plenty of people around.

Sign up with the National Cycle Database or Bike Register, both are free and help police return recovered bikes to their rightful owners.

Particularly important for electric bikes and high-value road bikes, which are increasingly targeted.

If you ever need to make a claim on your bicycle insurance policy, proof of ownership is essential. Keep a digital copy of your receipt, photos of your bike, and a note of the serial number.

Bicycle insurance isn’t compulsory, but with thousands of bikes stolen every year and nearly 15,000 cyclists injured on UK roads, being uninsured is a risk not worth taking.

For most casual riders and commuters, a home insurance policy with Theft & Loss and accidental damage add-ons does the job. Got a bike worth over £2,000? Add it as a high-value item and watch out for depreciation clauses and single-item limits.

For serious cyclists wanting personal accident cover, public liability cover, worldwide cover, or multi-bike discounts, a dedicated bicycle insurance policy from a specialist provider is the better option. Always check the policy wording before you commit.

No, bicycle insurance is not a legal requirement. But given how common bike theft is, and the potential costs of an accident, having proper insurance cover in place is strongly recommended.

Standard home insurance cover and most personal bicycle insurance policies won’t cover bikes used for business purposes, like courier or food delivery work. You’ll need a specialist commercial policy for that.

Check what an equivalent model sells for new (for new for old policies) or look at second-hand listings for the same make and model in similar condition (for market value policies). Don’t forget to factor in your accessories like helmets, lights, computers, and other kit all add up.

Most insurers will accept alternative proof of ownership, like a bank statement showing the purchase, a photo of the bike, or the serial number. Check your policy wording for what’s acceptable before you need to claim.

Public liability cover (sometimes called liability insurance or liability cover) protects you financially if you injure someone or damage their property whilst riding. It’s not legally required, but if you’re a regular cyclist, especially in busy urban areas, it’s well worth having.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.