Whether you own a brownstone in Brooklyn or a walk-up on the Upper East Side, when it comes to your homeowners insurance, empathy, speed, and trust matter.

Homeowners insurance financially buffers you, your family, and your stuff against bad things that could do some serious damage to your bank account. If a thief breaks into your home while you’re in the Caribbean or your grandma slips on your icy driveway, homeowners insurance has you covered.

What does New York homeowners insurance cover?

If you live in the Empire State, you know that summers are hot, winters are freezing, and seasonal storms are no joke so when it comes to your homeowners insurance coverage, you’ll want to protect your home from all sorts of potential risks and damage.

Dwelling

‘Dwelling coverage’ helps pay for damages to the structure of your home. So if your pipes burst next winter and damage your walls, or a windstorm blows over a tree and damages your home, you’re covered.

Other Structures

If one of the dangers mentioned above causes damage to your driveway, fence, shed, or other structures on your property, your homeowners insurance can help you out.

Loss of Use

If your place becomes uninhabitable due to covered damages, your ‘loss of use’ coverage can help pay for a temporary place to stay and basic living expenses such as food, laundry, parking, etc.

Personal Property

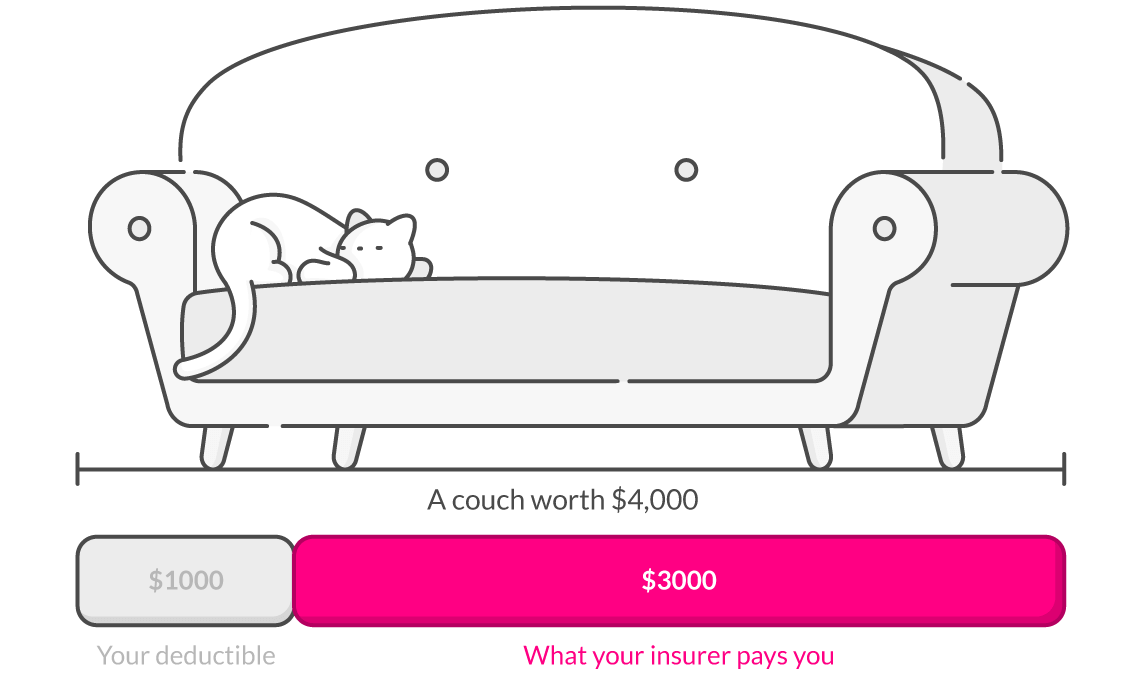

‘Personal property’ covers your stuff both inside and outside your home. So if your couch is ruined due to a burst pipe or your laptop is swiped at a coffee shop, homeowners insurance has your back.

Liability protection

If your neighbor slips and falls on an ice sheet on your driveway, you could be held liable. If someone is injured on your property, or anyone on your policy causes damage to someone else’s property or stuff, your insurance company should have you covered.

Medical Protection

If your neighbor needs to go to the hospital because of that slip and fall, your medical payments will kick in. Home insurance covers you if a guest gets injured at your place, or if you accidentally cause injury to someone outside your home.

Real-world homeowners insurance scenarios in New York

New York is its own category of risk. Nor’easters, aging brownstone plumbing, coastal storms on Long Island. Here’s what homeowners insurance actually covers when things go sideways.

Scenario 1: Burst Pipes in a Brooklyn Brownstone

It’s January. You went upstate for the long weekend. You come home Sunday night to a collapsed kitchen ceiling and two floors of water damage. Older brownstones, many built before 1940, have aging plumbing that’s especially vulnerable to hard freezes.

| Coverage | What it does |

|---|---|

| Dwelling coverage | Pays to repair your walls, ceilings, and floors. |

| Personal property coverage | Reimburses you for ruined furniture, electronics, and appliances. |

| Loss of use coverage | Covers your hotel and meals while repairs are underway, which matters when NYC hotel rates can run $250–$400/night. |

One thing to know: Burst pipe damage is covered, but a slow leak you ignored for months usually isn’t. The sooner you document and report, the better.

Scenario 2: Nor’easter damage on Long Island

A named storm rolls in off the Atlantic. By morning, your roof has taken a hit, siding is peeling, and there’s water in your living room.

| Coverage | What it does |

|---|---|

| Dwelling coverage | Covers wind damage to your roof, siding, and windows, and water that entered through that damage. |

| Flood damage | Not covered under a standard policy. Storm surge or rising floodwater from outside requires separate flood insurance. |

One thing to know: Named storms may trigger a separate deductible, typically 1–5% of your dwelling coverage. On a $500,000 home, that’s $5,000–$25,000 out of pocket before coverage starts. Know your deductible before storm season.

Scenario 3: Theft in a Manhattan or Brooklyn apartment

You’re traveling. Someone breaks in and takes your laptop, camera gear, and an engagement ring.

| Coverage | What it does |

|---|---|

| Personal property coverage | Covers your belongings inside and outside your home, including a laptop stolen at the airport or a bike taken from outside your building. |

| Sub-limits to watch for | Jewelry, art, and musical instruments often have coverage caps. If your ring is worth $8,000 and your policy caps jewelry at $2,500, you’re covering the difference. |

| Extra Coverage | Scheduled personal property lets you insure specific valuables at their full appraised value, and covers accidental damage, not just theft. |

One thing to know: A home inventory, including photos, receipts, and serial numbers, makes the claims process significantly faster.

Scenario 4: A guest gets hurt at your Queens home

You’re hosting a backyard party in Astoria. A friend trips on a loose step, fractures their wrist, and faces $4,000 in hospital bills.

| Coverage | What it does |

|---|---|

| Medical payments coverage | Handles immediate medical expenses, typically $1,000–$5,000, without requiring your guest to file a lawsuit. |

| Personal liability coverage | Steps in if it escalates legally, covering defense costs and settlements up to your policy limit. |

One thing to know: If you own significant assets, a home, retirement savings, investments, your liability coverage protects those too. If $100,000 isn’t enough, an umbrella policy adds $1M or more on top.

Scenario 5: Fire damage in a multi-family Bronx home

A fire starts in a neighboring unit and spreads to yours. Structural repairs alone run over $200,000.

| Coverage | What it does |

|---|---|

| Replacement cost coverage | Pays what it actually costs to repair or rebuild, regardless of depreciation. In NYC, where construction costs have risen sharply, this matters a lot. |

| Actual cash value | Accounts for depreciation, so a 10-year-old kitchen gets reimbursed for what it’s worth today, not what it costs to rebuild. |

| Loss of use coverage | Covers temporary housing and additional living expenses, including food, laundry, and parking, while repairs are underway. |

One thing to know: If repairs require bringing your home up to current building codes, common in older NYC buildings, you may need Ordinance or Law coverage. Standard policies may not cover code upgrade costs automatically.

Scenario 6: Accidental damage to a neighbor’s property during renovation

You’re renovating your kitchen. A contractor accidentally damages your neighbor’s wall, or a pipe they disturb floods the unit below.

| Coverage | What it does |

|---|---|

| Personal liability coverage | Can cover property damage you, or people working in your home, accidentally cause to others, including legal fees if your neighbor decides to sue. |

| What’s not covered | Intentional acts are excluded. If a contractor’s direct negligence caused the damage, their general liability policy should respond first. |

One thing to know: Always verify your contractors are licensed and insured in New York before work starts.

How much is home insurance in New York?

According to Value Penguin, homeowners in New York pay around $969 per year on average for home insurance, compared to the national average of $2,151.

There’s no standard policy price when it comes to homeowners insurance. Your college friend who lives in Long Island will have a totally different price than your cousin who owns a penthouse on the Lower East Side.

| City | Average annual cost of homeowners insurance |

|---|---|

| New York | $2,495 |

| Buffalo | $1,100 |

| Rochester | $1,050 |

| Yonkers | $1,460 |

So, what variables impact your home insurance cost?

- Location of your home

If you live in a high-risk area for theft, fire, or windstorm, your policy will be pricier than it would be if you live in a low-risk area.

- Age of dwelling

If your home is brand new, you could get a discount on your homeowners insurance policy. However, old buildings are more likely to have structural issues or problems with the electrical or plumbing systems, which may hike up the price of your insurance a bit.

- Protective devices

If you have a fire alarm you could get a discount on your homeowners insurance. That’s because they’ll allow you to prevent a fire before it becomes an issue.

- Amount of insurance

The cost to rebuild your home has a big impact on the price of your policy. If your home is on the large side, or made of expensive materials, your home insurance policy might be a bit pricier.

- Deductible

The lower your deductible, the higher your homeowners insurance price. So choose a deductible that makes the most sense for your lifestyle.

- Add-Ons

If you add your expensive jewelry or fine art or tack on water backup coverage to your policy, your price will go up a bit.

- Claims history

If you’ve never filed a claim, you’ll probably have a cheaper homeowners insurance policy than someone who has a history of filing claims.

Why get Lemonade homeowners insurance for New York?

Lemonade is powered by tech, so you can get a policy on the Lemonade app in less than 5 mins – zero paperwork, zero hassle.

If you ever need to file a claim, Lemonade can process them instantly, handling 30% in 3 seconds. Lemonade also does not use brokers, making each policy cheaper than competitors.

Lemonade is built around a simple idea: insurance should take care of people when they need it most, and do some good along the way.

When you get your first policy, you choose a cause you care about, and Lemonade donates to nonprofits supporting those causes. More customers choosing a cause means larger donations to nonprofits supporting it.

Giveback is at the heart of how Lemonade works. When everyone knows that your insurance connects to causes people care about, it creates a system where honesty, fairness, and trust naturally come through, especially when it’s time to file and handle claims.

How much home insurance do I need in New York?

When it comes to home insurance, most people know they need it, but make the mistake of purchasing too little. Your home insurance comes with six broad areas of coverage, touching upon various scenarios having to do with damages and losses to your property/residence, yourself, and others. We’ll break that down in the sections to come, and how much coverage you need in each category, so you’re properly protected against every scenario. Read more here.

Dwelling coverage

Dwelling Coverage protects you from damages to your place (your home and everything attached to it, such as a garage, chimney, in-ground pool, etc.) When it comes to setting a dwelling coverage amount for your home, you don’t want to choose the purchase price or current market value. It should be the amount that it’d take to rebuild your home (as it was before the damage), known as “reconstruction costs.” This is what your insurance company will be reimbursing you for in the worst-case scenario that you have to rebuild.

Personal property coverage

Personal Property is insurance lingo for “your stuff” (bikes, laptops, TVs, etc.) To determine how much personal property coverage you should get, choose a limit between 50 – 75 percent of your dwelling coverage amount. If you don’t think this covers all your stuff (including your priciest purchases) look into the Extra Coverage option with your insurer. Extra Coverage, also known as scheduled personal property, this add-on covers everything listed on your base policy, plus additional types of accidental damage.

Loss of use coverage

Loss of Use helps with temporary living expenses if your place becomes unlivable due to a peril like a fire, mandatory evacuation, etc. Similar to personal property, additional expenses, or loss of use, is also based off of dwelling coverage. You should choose an amount that’s around 20-30 percent of your dwelling coverage. Also, take your lifestyle into consideration, as this covers what you’d usually spend on stuff like food, temporary storage of property, moving costs, etc. So let’s say you eat takeout everyday – breakfast, lunch, and dinner, you’ll most likely want to select an amount that’s more than someone who buys groceries and prepares their meals.

Personal liability coverage

Personal Liability refers to bodily injury or property damage to other people (or their stuff) as a result of your actions, at your home, and anywhere else. Personal liability, might just sound like legal fees, you may only think of the things we discussed above (injury to others, legal fees, etc.), but you should also take into account the total dollar amount of your financial assets, like your home, retirement accounts, investments, and anything else worth money. Your insurer’s liability coverage is also working to cover these things as well. If you don’t think $500K is enough, you can purchase something called an umbrella policy which will add another $1M or more in coverage.

Medical payments to others coverage

Let’s say a guest sprains her wrist after tripping on a rug in your living room, and she has hospital bills to pay. This is where your medical expenses coverage may kick in. You should generally choose between $1,000 – $5,000, but really depends on you. Try looking at how often you host and the safety of your home.

Home insurance in New York FAQs

Is homeowners insurance required in New York?

New York State doesn’t legally require homeowners insurance. But if you have a mortgage, your lender almost certainly does — it’s a standard condition of the loan. And even if you own your home outright, going without insurance means you’re personally responsible for every dollar of damage, liability, or loss. Given New York’s weather risks, theft rates, and legal environment, most homeowners find that coverage costs a lot less than the alternative.

What are the different types of homeowners insurance?

Lemonade offers two types of home insurance policies: one for single-family homes, (called HO3 in insurance-speak), and one for condos (HO6). There are minor differences between the two, and you’ll choose the right policy depending on the type of home you’re looking to insure. In a nutshell, whereas homeowners own and are responsible for everything on their property, (home, garage, fence, etc.), condo owners with HO6 policies are only responsible for the outermost walls of their unit, inward.

How can I save on homeowners insurance in New York?

A few things can bring your premium down:

- Install safety devices: smoke detectors, a burglar alarm, or a water leak sensor can all lower your rate.

- Weatherproof your home: storm shutters, updated plumbing, or new electrical systems may qualify for a discount. Ask your insurer what counts.

- Raise your deductible: the higher it is, the lower your premium. Just make sure it’s an amount you could cover if you needed to.

- Answer a few questions in the app: Find discounts based on your home’s safety setup and any renovations you’ve made.

Does homeowners insurance cover flood damage in New York?

No, standard homeowners insurance does not cover flooding. This catches a lot of New Yorkers off guard, especially after a nor’easter or heavy rain event. Flood damage from rising water, storm surge, or overflow requires a separate flood insurance policy, available through the National Flood Insurance Program (NFIP) or a private insurer.

Does homeowners insurance cover theft in New York City?

Yes. Personal property coverage includes theft of your belongings, both inside your home and away from it. So if your laptop gets stolen at a coffee shop or your bike disappears from outside your building, you’re covered up to your policy’s personal property limit.

High-value items like jewelry, cameras, or musical instruments may have sub-limits under a standard policy. If you have valuable items worth more than those limits, Extra Coverage (scheduled personal property) lets you insure them at their full appraised value.

What does loss of use coverage pay for in New York?

If your home becomes uninhabitable after a covered event, like a fire, burst pipe, or storm damage – loss of use coverage pays for your temporary living expenses while repairs are underway. That includes a hotel or short-term rental, meals, laundry, parking, and other costs above your normal spending.

In New York City, where hotels can run $250–$400 a night and short-term rentals aren’t cheap, this coverage can make a real difference during what’s already a stressful situation. Most policies set loss of use at around 20–30% of your dwelling coverage amount.

Reddit asked, we answered

What's the best homeowner insurance for Brooklyn?

At Lemonade, we cover Brooklyn homeowners with fast claims through the app, transparent pricing, and coverage for urban risks like theft and vandalism. We operate in New York and our digital-first approach means no paperwork headaches. Get a quote specific to your Brooklyn address and property type. Read the full thread on Reddit

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share