Engagement Ring Insurance: What’s Covered & How It Works

Everything you need to know about insuring your engagement ring against loss and damage.

Everything you need to know about insuring your engagement ring against loss and damage.

Navigating the world of engagement rings involves more than just picking the perfect gem. Once you’ve found that dazzling symbol of love, it’s crucial you take the steps to protect it.

This is where engagement ring insurance becomes your best friend. Whether you’re planning a romantic getaway or simply living your daily life, having the right coverage can provide peace of mind and protect your precious investment. By adding it to your homeowners insurance, you safeguard against unexpected loss or theft.

Let’s break down everything you need to know to make sure your engagement ring is well-protected.

TL;DR

TL;DR

Once you’ve decided to get coverage for that sparkler, you’ll want to consider a few different options. After all, getting insurance for an engagement ring deserves at least some of the consideration you had when you picked it out.

The first option is to add your diamond ring to your renters or home insurance policy. Most insurers have max amounts (referred to as limits of liability) that cap off how much coverage is automatically included for valuable items like engagement rings.

At Lemonade, $1,500 worth of jewelry is insured in the base plan for theft. In other words, the total cost of all your jewelry is covered only up to $1,500 if someone comes in to take your stuff. If you only have a simple engagement ring, $1,500 in coverage is probably enough to replace the band.

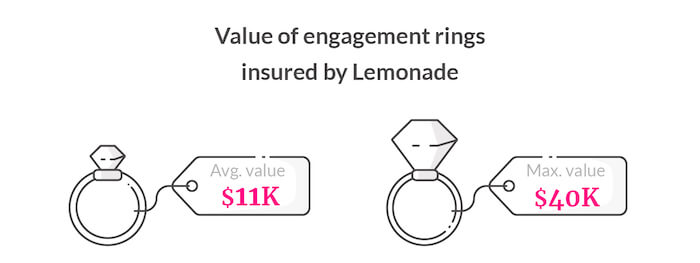

In general, diamond rings might require additional coverage. In 2018, the average price of an engagement ring added to Lemonaders’ policies was $10,902, so you should go ahead and assume you’ll need to add Extra Coverage (sometimes called scheduling) for your glittery diamond engagement ring.

Best part? At Lemonade, you won’t have to pay a homeowners insurance deductible for anything scheduled as a personal property endorsement (aka, Extra Coverage). So if your $12,000 ring mysteriously disappears, Lemonade can pay you up to the full replacement cost, deductible-free!

Extra Coverage on your renters or homeowners insurance policy protects your ring against most unexpected events. Here’s what’s covered and what’s not:

At Lemonade, Extra Coverage insures you for just about anything, except general wear and tear. So if your white gold band is starting to look dull, you can’t file a claim to get it redipped.

Different insurance companies use different language in their policies, so always check your actual policy documents. At Lemonade, Extra Coverage protects against just about anything unexpected, as long as it’s not normal wear and tear.

There are two ways your insurance provider can pay you after they approve your claim: actual cash value or replacement cost. The difference can be huge.

What it means: The “Amazon price” – what it costs to buy something new today

How it works: You get the full amount to replace your ring, regardless of age

Example: Your 3-year-old $8,000 ring gets stolen → you get $8,000 to buy a new one

At Lemonade: We offer replacement cost up to $40,000 for engagement rings and up to $25,000 for other jewelry. Our customers’ engagement rings average around $11,000 in value.

What it means: The “eBay price” – what your used ring is worth today

How it works: Original cost minus depreciation

Example: Your 3-year-old $8,000 ring gets stolen → you might get $5,000-6,000

Why Lemonade uses replacement cost: Diamond jewelry replacement cost is usually much higher than cash value, so our replacement cost coverage puts you in a much better position.

Another thing to watch out for: some insurance companies require you to repair or replace your ring at specific locations – even if your ring is custom.

At Lemonade: You decide where and how to spend your approved claim money

Other companies: May force you to use their chosen jewelers or repair shops

To get Extra Coverage for your engagement ring, you’ll need proof of its value:

It’s official documentation that confirms your ring’s current value. Different insurance companies have different standards for appraisals, but at Lemonade, we accept appraisals from any licensed jeweler.

Appraisal requirements:

So if you’re adding your grandmother’s ring in June 2025 but only have an appraisal from 2019, you’ll need to get it updated. You can choose any jeweler, but for peace of mind, we recommend using a certified Gemologist who can provide the most accurate jewelry appraisal for your ring.

The cost of insurance can vary significantly, depending on your home’s location and the replacement cost of your engagement ring.

If your ring would cost $7,000 to replace, you would expect to pay between $70-$140 dollars every year, or between $6-$12 a month in coverage, on top of your usual premiums. You’ll be able to see the costs broken down in simple terms on your declarations page. (BTW, here’s a behind-the-scenes guide to how much homeowners insurance costs.)

Adding Extra Coverage for an engagement ring to your Lemonade policy is simple – just follow these steps:

1. When you’re getting your Lemonade policy, tap ‘Activate Extra Coverage.’ If you already have a policy, head to the Lemonade app and tap the Extra Coverage button under ‘Add-Ons.’

2. Open up the email you get from Maya, and click ‘Add Extra Coverage’

3. Go through the flow, and send over a picture of:

“Snapping a few pics is easy and quick! This info is incredibly important to make sure we’re properly insuring your stuff. It also makes your claims process much smoother if something were to happen. We’ll already have all the docs we need on file – so it’s less work for you down the road!” – Ashley Delgado, Lemonade Customer Experience Specialist

4. Our CX team will get back to you, and let you know via email once your ring is covered! Btw, you can always add on more items later.

A couple of notes here:

Lemonade offers temporary Extra Coverage for 14 days while you get all your pictures in order or wait for an appraisal.

To get temporary coverage, make sure to answer ‘Yes’ when AI Maya asks if you have any valuable items. Then, select which items you’d like to insure under Extra Coverage in the Lemonade app.

Provide a guesstimate of the value of the ring you’d like to cover (refer to step 1), and Lemonade will automatically grant you temporary Extra Coverage! (In the unlikely event of a claim, you will still need to prove it existed, what it was worth, and that you had it when you bought the policy.)

This will give you time to send over the necessary info and for our CX team to review it. Don’t forget, this temporary Extra Coverage will last for 14 days, so try to submit your info by then. If you can’t get to it, you can still add on the Extra Coverage yourself after it expires.

Here’s a guide to everything you need to know about Extra Coverage. Have more questions about Extra Coverage? Open up your Lemonade app, and ask AI Maya. Or shoot an email over to [email protected], and our CX team will get back to you as soon as possible.

One of you paid for the ring, and the other probably gets to wear it. One of you inherited the center stone, and the other paid for the band. You split the cost, and it’s been sitting in a jewelry box for 6 months. Who should be insuring this ring anyway? Does one policy cover both of you?

Once you’re married, you’re considered related, so you’re both automatically covered under your homeowners insurance policy.

Adding your spouse to your plan is easy, and it won’t cost you a dime! They’ll be considered a “Named Insured,” which is insurance speak for someone who is implicitly included in the policyholder’s plan.

Haven’t made it down the aisle yet? We’re sure your love transcends labels, but when it comes to insurance, your marital status does matter.

If you’re living with a significant other, add your partner to your insurance policy as an ‘additional insured.’ Because if he or she loses the engagement ring while in their possession, it’ll only be covered if their name is on your policy.

So, who should be covered? The person who has the ring needs to have his or her name on the policy.

Who has the ring? If it’s sitting in a drawer waiting for the anniversary of your first kiss when it gets stolen during a break-in, whoever bought the ring will need to have insurance coverage. If it falls off and rolls away during a girls’ night out, you’ll want to make sure the wearer is covered, too.

In addition to insuring your engagement ring, there are practical ways to protect it from damage and loss.

It’s recommended to avoid wearing your ring during activities where you could potentially harm your ring, or lose it-such as working out, gardening, or even your skincare routine. If you want to err on the side of caution, check out these 10 things you should never do while wearing your engagement ring.

Keeping your engagement ring clean is equally important. Regular at-home cleaning in addition to annual professional care can help keep your ring sparkly, plus it can help prevent the loss and loosening of stones. Want to learn more about engagement ring cleaning etiquette? Head to our complete guide on how to clean your engagement ring like a pro.

The truth is, you don’t need a diamond to shine, but when your jewelry is as valuable and meaningful as an engagement ring, you’re going to want to protect it. It’s easier and more affordable than ever! Using AI and machine learning, Lemonade’s insurance policies are much lower than the industry average.

You need proof of your ring’s value, either a recent receipt (if you bought it) or a jewelry appraisal (if it was inherited or a gift). At Lemonade, appraisals must be dated within five years of when you apply for coverage.

Your engagement ring is covered worldwide under Extra Coverage. Whether you lose it at home, on vacation, or anywhere else, you’re protected for the full replacement value.

Extra Coverage on your homeowners or renters insurance policy protects your ring against most unexpected events. Here’s what’s covered and what’s not:

Yes! Unlike some insurers that require you to use specific jewelers, Lemonade lets you decide where and how to spend your claim money. This is especially helpful for custom or personalized rings.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.