What is a Multi-driver Car Insurance Policy?

Who should I cover to drive my car? And how will covering multiple drivers on my policy affect my premium?

Who should I cover to drive my car? And how will covering multiple drivers on my policy affect my premium?

If someone in your home drives your car regularly, they need to be on your policy. That’s the short answer.

The longer one: multi-driver car insurance lets you cover everyone under your roof on a single policy: your spouse, your teen, your roommate who “just needs it for one errand.” At Lemonade Car, you can add up to seven drivers, right from the app.

Not sure who you need to cover, or how adding drivers affects your premium? Let’s get into it.

TL;DR

TL;DR

Multi-driver car insurance is there to protect your car, and your loved ones who regularly take it for a spin.

It’s pretty simple: When you’re building your car insurance policy, you add all the drivers that you want covered to drive your car.

You’re able to cover multiple family members (or your trustworthy roommates) to drive your car under a single policy. Keep in mind that your car insurance company may have a limit on how many drivers you can add to your policy. At Lemonade Car, we limit it to seven drivers per policy (depending on your state).

Don’t forget, though: On a single policy, you can only cover cars that are registered under your or your spouse’s names, and that are registered and garaged in the same state.

Most coverages that you include on your Lemonade Car policy are geared towards the cars themselves, not each driver that gets behind the wheel. In other words, if your car is involved in an accident, your coverage will depend more on the car involved than on which driver from your policy was in the driver’s seat when it happened.

For example, when you include certain coverages on your car, like comprehensive coverage and collision coverage (which are different, but both really important), anyone listed on your policy who’s driving that car could be covered for things like a crash with another vehicle, or with a deer.

Just a refresher: All cars on your Lemonade Car policy will have to carry the same liability coverage-the bare minimum car insurance that covers damage you may cause to other drivers and their property. But beyond that, our add-on coverage options are super customizable. Plus, if you drive with the Lemonade app, we’ll include roadside assistance, on us.

Yes! Most car insurance providers will let you cover up to four drivers, but at Lemonade Car you can include up to seven drivers on your policy.

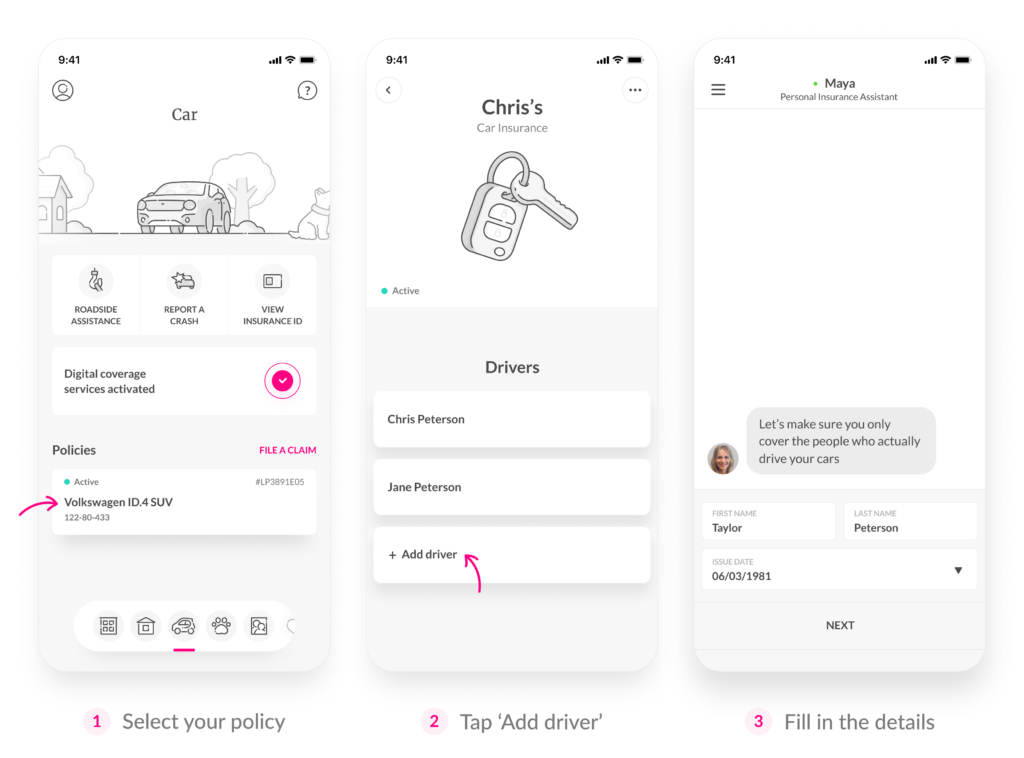

You can easily cover multiple drivers when you build your Lemonade Car policy on the Lemonade app (available for iOS and Android) or on our website.

Need to cover an additional driver on your policy once your term has already started? No problem! You can add drivers to your existing policy at any time, all through the Lemonade app. Keep in mind that adding more drivers to your policy may impact your car insurance premium (but we’ll expand on that later).

Technically, you can cover just about any licensed driver on your policy, but there are certain people that you need to cover before they can get behind the wheel of your car.

If someone meets these 3 criteria, you need to include them on your policy:

There may be a lot of different people in your life who you should cover on your car insurance policy. Let’s take a spin through a few of the most common scenarios.

You and your spouse share a lot of things: vows, plans for the future, a bed, and car insurance. When it comes to car insurance coverage, there’s no need for your spouse to have a separate policy. Just make sure to add them as a driver on yours.

There are so many perks that come along with carrying a single car insurance policy with your spouse, like having one quote, one policy document, and one renewal date for all the cars you need to cover. What’s more romantic than organization and efficiency? That was rhetorical…

You’ll also be eligible for a multi-car discount if you and your better half need to cover more than one car on your policy. Together you can cover up to four cars that are registered under either of your names on a single policy.

But what if you and your spouse have different driving records? Say you’ve got a clean record and your spouse picked up a speeding ticket a couple of years back. Does it still make sense to share a policy?

Yes, and not just because you’re required to add them anyway. A single household car insurance policy is almost always simpler and more cost-effective than two separate ones. Your spouse’s driving history will factor into your premium, but Lemonade Car looks at the full picture, including how everyone on the policy actually drives.

And whatever you do, don’t skip adding them altogether. If your spouse regularly drives your car and isn’t listed on your policy, a claim involving them could be denied.

As soon as your teenager gets their learner’s permit you can add them to your policy with no additional charge.* But let us know when they get their full-fledged driver’s license and officially join the fleet.

It’s true: Having a young, licensed driver on your policy will impact your premium. But with Lemonade Car, they’ll have the chance, every policy term, to prove their safe driving habits (and get you better rates when they do).

If your youngster drives their own car, it would have to be registered under your or your spouse’s name (and registered and kept in the same state) to be covered by your policy.

Here’s a question we hear a lot: how much more does adding a teen driver actually cost? There’s no way around it, teen drivers typically increase premiums because of their lack of experience. But the increase isn’t permanent. At the end of each policy period, your teen has the chance to show their safe driving habits through the Lemonade app, which can bring real savings over time. Think of it less as a penalty and more as a starting point.

Your kid’s home from school for the summer and needs the car to get to their part-time job. Seems straightforward, but whether you need to add them to your policy depends on one key question: where do they actually live?

If they’re back under your roof for the summer, have their license, and are using your car regularly, they meet all three criteria and need to be on your policy. If they’re primarily living at school and only home for a few weeks, it’s less clear-cut. Reach out to us and we’ll help you figure out the right call.

The good news: if they go back to school and no longer have regular access to your car, you can remove them from the policy. They’ll only factor into your premium for the time they were listed.

Mom or dad is moving in. They still have their license and plan to drive occasionally, maybe to appointments or the grocery store. Do they need to be on your policy?

If they’re living in your home, have a driver’s license, and will have regular access to your car, yes. They need to be added as a driver. It doesn’t matter if they only drive once a week. Regular access is the threshold, not how often they actually use it.

You trust your long-term partner or roomie to water your plants while you’re on vacation. But you shouldn’t trust them with your car unless they’re covered on your auto insurance policy.

Even if they’re a safe driver and only heading a few blocks away, it’s not worth letting an uninsured driver take your car for a spin, because they might not be covered in the case of a crash.

Let’s say you regularly let your roommate Chad take your Prius for weekend trips. He’s not listed on your Lemonade Car policy. On the way to Bonnaroo he rear-ends a farm truck carrying a ton of heirloom tomatoes. Guess what? The damage to your vehicle (and to the truck, plus any liability for injuries) probably wouldn’t be covered by your policy.

If your babysitter is frequently using your car to pick your kids up after school, or someone is borrowing your car while they look after your home (or cats) during your extended vacation, you should include them as a driver on your Lemonade Car policy.

What if this is just a temporary situation? Well, you can contact us at any point to remove them from your policy. Then the driver that you covered temporarily will only impact your premium for the amount of time they were listed on your policy.

If you drive for a rideshare platform on the side, it’s worth knowing that standard personal car insurance (including Lemonade Car) typically doesn’t cover you while you’re on the clock. The moment you activate the rideshare app, you’re using your car for commercial purposes, and that usually falls outside the scope of a personal auto policy.

Most rideshare platforms provide some coverage while you have an active passenger or accepted ride, but there’s often a gap between when you open the app and when you accept a trip. So if this is a regular part of how you use your car, it’s worth factoring that into your coverage decisions.

Insurance has a way of making simple things sound complicated. Here’s a plain-language breakdown of the terms you’ll run into when building a multi-driver policy, and how different coverage options stack up.

“Regular access” means someone can use your car whenever they want, not just in an emergency or one-off situation. Think: your partner has a key, or your teenager can grab it and go. If someone has easy, ongoing access to your car, that counts, even if they don’t use it all the time.

A household member is anyone who lives in your home and has a driver’s license. Doesn’t matter if they’re family or a roommate, if they live with you and could drive your car, they need to be listed on your policy. Household members’ coverage is baked into how multi-driver policies work: the policy follows the home.

An excluded driver is someone you’ve explicitly removed from coverage on your policy, by signing a form stating that the person is excluded. This can happen if a household member has a driving record so poor it would make your premium unworkable. But it’s a serious move, if an excluded driver gets behind the wheel and gets into an accident, nothing is covered. And not every state allows driver exclusions, so availability varies.

Named drivers are the people explicitly listed on your policy, specifically your declaration page, as covered to drive your car. At Lemonade Car, you can name up to seven drivers on a single policy. Each named driver’s history and habits factor into your premium.

Permissive use means you’ve given someone permission to drive your car, even if they’re not on your policy. Some policies extend limited coverage in these situations, like a genuine one-time emergency, but it’s not something to count on. If someone has regular access to your car, permissive use isn’t a substitute for adding them properly. An unlisted regular driver is a coverage gap waiting to happen.

Not sure which option fits your situation? Work through these:

When you’re adding drivers to your Lemonade Car policy, we’ll ask for things like their:

At Lemonade Car, we need up-to-date and accurate information on all the drivers you include on your policy to help us determine the fairest car insurance quote. Keep in mind: Some people might not be eligible to be added to your policy depending on their driving record and other factors.

Adding another driver to your Lemonade Car policy could help or hurt your insurance rates depending on a lot of factors-like their driving history and claims history. While covering a spouse or significant other with a spotless driving record might help you score lower rates, having an inexperienced, young driver on your policy may have the opposite effect.

But there are so many ways you can lower your car insurance costs-like driving with the Lemonade app, or bundling your Lemonade car insurance policy with Lemonade renters, homeowners, pet, or term life insurance. When you have more than one car to cover, you’ll also be eligible for a multi-car discount.

At Lemonade Car, the way you actually drive matters. We reward low-mileage drivers and drivers that consistently prove their safe driving habits with serious savings. Everyone that you cover will have the chance, during every six-month term, to show they’re the safest driver on your policy.

Yes! Your Lemonade Car policy will be under your name, and each driver you include will be part of that coverage.

When you add another driver to your policy, we’ll ask you for their mobile number so we can send them a link to join the policy. Once they download the Lemonade app on their own phone from the link and make a profile, they’ll be ready to see the policy and take your car for a spin (with your permission of course).

No matter how many drivers are listed on your policy, the only name that you’ll usually see on your Lemonade insurance ID is your own (but this varies by state). That’s because the car(s) being covered on the policy are registered under your name.

If you’re covering multiple cars on your policy, and at least one of them is registered under your spouse’s name, the ID will include both of your names.

Your Lemonade insurance ID is still a totally valid document for any other driver that’s covered on your policy to use as proof of insurance, even if their name isn’t on it.

So, what’s the best car insurance when you need a multi-driver policy? Glad you asked. We’re a bit biased, but… when you cover your loved ones-or your ex-boyfriend that’s still sleeping on your couch-with Lemonade Car, you can enjoy great coverage, score savings and discounts, and help make the planet a little greener for generations to come.

Ready to take Lemonade Car for a spin? Click the button below to get your quote.

Three things trigger the requirement: they live in your home, they have a valid license or learner’s permit, and they have regular access. Hit all three? Add them to your policy.

Up to seven in most states. Most insurers cap it at four, but Lemonade lets you cover up to seven drivers on one policy.

Not great news: your insurer could deny the claim. If your roommate lives with you and regularly uses your car, they need to be listed, full stop.

Yes, and you should. Spouses belong on the same policy, regardless of driving history. Their record will factor into your rate, but that’s true at any insurer.

If they’re driving your car while they’re home, yes, add them. You can always update your policy when they head back to school.

It could go either way. A clean, long driving history is generally a positive signal. But age and specific driving record details will both factor into how your rate is calculated. There’s no guarantee it’ll bring your price down.

You’ll need their full legal name, date of birth, relationship to you, and driver’s license number. That’s it, then the app walks you through the rest.

A named driver is someone explicitly listed on your policy, they’re covered every time they drive your car. Permissive use is what kicks in when someone not on your policy borrows your car occasionally, with your permission. The key word is “occasionally.”

That’s actually normal. Your policy is in your name, and your ID card reflects that, but your spouse is still covered as a listed driver. The ID card isn’t a full list of everyone on the policy.

Yes. You can add and remove drivers through the Lemonade app any time, mid-term changes are no problem. Just keep in mind: if someone drives your car regularly, they need to be on your policy while they’re doing so.

An excluded driver is someone you’ve specifically named on your policy as not covered, meaning if they drive your car, your insurance won’t pay out. People usually do this to keep premiums lower when a household member has a rough driving record.

Yes, everyone on your policy should have the Lemonade app on their own phone. It’s how they access the policy, unlock driving perks, and stay covered properly.

A few quick words, because we <3 our lawyers: This post is general in nature, and any statement in it doesn’t alter the terms, conditions, exclusions, or limitations of the policies issued, which differ according to your state of residence. You’re encouraged to discuss your specific circumstances with your own professional advisors. The purpose of this post is merely to provide you with info and insights you can use to make such discussions more productive! Naturally, all comments by, or references to, third parties represent their own views, and Lemonade assumes no responsibility for them. Coverage may not be available in all states. Please note that statements about coverages, policy management, claims processes, Giveback, and customer support apply to policies underwritten by Lemonade Insurance Company or Metromile Insurance Company, a Lemonade company, sold by Lemonade Insurance Agency, LLC. The statements do not apply to policies underwritten by other carriers.

Share

Please note: Lemonade articles and other editorial content are meant for educational purposes only, and should not be relied upon instead of professional legal, insurance or financial advice. The content of these educational articles does not alter the terms, conditions, exclusions, or limitations of policies issued by Lemonade, which differ according to your state of residence. While we regularly review previously published content to ensure it is accurate and up-to-date, there may be instances in which legal conditions or policy details have changed since publication. Any hypothetical examples used in Lemonade editorial content are purely expositional. Hypothetical examples do not alter or bind Lemonade to any application of your insurance policy to the particular facts and circumstances of any actual claim.